In early 2023, we witnessed huge volatility in the US Regional Banks that is likely to lead to an extended period of consolidation. A key issue, brought to the forefront of the market’s attention in March, is that bank assets and liabilities are at an extreme duration mismatch.

Balance sheets are filled with long-duration, low-yielding fixed income securities and loans, while liabilities can be shorter-term than previously anticipated. As interest rates rose, the value of their assets declined substantially. The issue was exaggerated where large portions of bank assets were classified as “held-to-maturity” and were not marked to market. This artificially made the assets of some bank balance sheets look financially better than they actually were. Some banks also had an outsized percentage of their deposits uninsured by the FDIC, compounding the problem. These banks, with suspect liquidity, experienced significant deposit outflows, culminating with the headline failures of Silicon Valley Bank, Signature Bank, and First Republic Bank.

It was at this point that the Federal Reserve and the Treasury Department alleviated the short-term liquidity squeeze on the banking industry. They provided an implied FDIC guarantee on all bank deposits to stop runs on the banks, created the Fed Bank Term Funding Program (BTFP) to assist banks having liquidity issues, and helped arrange a number of bank acquisitions by larger banks. These measures effectively stabilized the short-term liquidity issues within the industry. The question now is whether these measures were a short-term fix or a longer-term solution. Significant issues persist within the banking sector concerning the quality of their balance sheets, which in some cases have deteriorated further due to rising interest rates and bank’s decreased ability to generate profit.

Duration Mismatch Remains Unresolved

A key concern is that for some banks the duration mismatch of assets and liabilities has not gone away. Some banks have sold some of their long duration securities at losses to reduce their interest rate risk, but most bank assets are still loans. With very few people paying off their mortgages or refinancing their maturing debt, the average duration has been lengthening considerably due to the low rates that were prevalent when these loans were taken out. Simultaneously, the regional banks are experiencing the largest contraction in deposits in decades.

Competition for client deposits from new providers like Apple, other banks, money market funds, ETFs or broader fixed income alternatives has forced regional banks to continue to gradually increase deposit rates. However, the increase in the average securities yield of banks’ portfolios has often remained muted.

Depositors are increasingly waking up to the new reality that excess cash balances can generate return, resulting in a stampede out of non-interest-bearing accounts into higher yielding alternatives. Higher rates aren’t just impacting the liability/deposit side of bank balance sheets but the asset side as well. When interest rates rise, the market value of fixed income securities and loans decline.

Commercial Real Estate Concerns

A big concern for investors is focused around Office and Commercial Real Estate (CRE), especially office and retail properties in central business districts. Commercial office real estate is being hit by the shift to remote work. Large vacancy rates are reducing cash flows at a time when many loans will have to be renewed at substantially higher rates. Some industry experts are forecasting material losses in the value of commercial office real estate in many of the central business districts. This would result in many borrowers choosing to hand the keys to the bank rather than doing a ‘cash-in' refinancing.

As the potential stress in the commercial real estate pipeline continues to build, it will take time before losses show up on bank balance sheets. This will likely impact aggregate economic activity over the next 12 months.

One area of the regional bank loan market that has yet to garner much attention is the traditional commercial and industrial space. Commercial loans typically carry a variable interest rate and are underwritten based on the underlying cash flows of the organization, or collateralized by equipment value. With each passing month, commercial borrowers face incremental pressure as their interest expense increases while the current disinflationary real estate environment pressures margins and collateral values. Most commercial loans were underwritten in an environment where companies’ income statements were healthy due to lower expense bases and higher fiscal support in the form of COVID relief. U.S. Chapter 11 bankruptcy filings have increased 68% in the first half of 2023 compared to a year earlier. The resilient US consumer aside, with interest rates set to remain high for some time, small business default rates are likely to continue to move higher.

While there are many regional banks that have outsized CRE exposures, regulatory controls have limited the percentage of a regional bank’s capital that can be exposed to CRE. However, there are no limits to a bank’s exposure to commercial credit. Many regional banks that have been in the news for CRE risks have only 20% of their loan book in CRE with more than 50% of their loan book in commercial lending.

Unless interest rates drop dramatically, we are likely to see more regional banks under stress and further subsequent consolidation. Some banks will be negatively impacted by their asset liability mismatch and credit portfolios. Others will excel, benefitting from superior credit profiles and diversified business models that permit them to take advantage of market dislocation to gain market share.

During this period of change, it is important to note that there are vast differences in the quality of banks as well as diverse operating models which will result in broadly varied outcomes. These nuanced differences are will not be fully appreciated by many investors and are may not reflected in stock prices, thereby making the sector opportunity-rich.

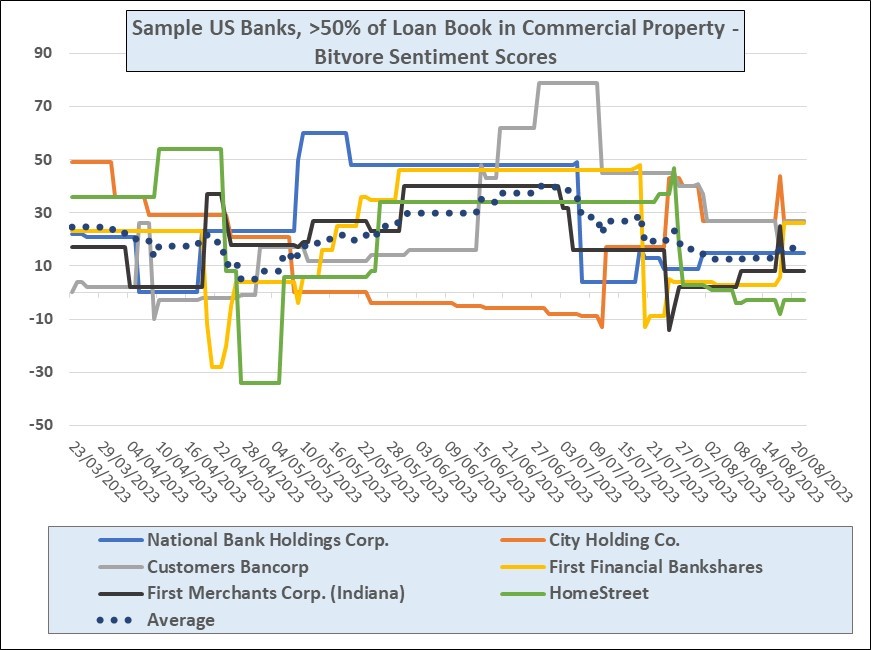

As we did in our May report on regional banks, we have plotted the daily Bitvore Sentiment Scores for a sample of small US Banks whose loans books are estimated to be over 50% exposed to US commercial property.

Miss Nothing With Bitvore's Automated Intelligence

Trusted by more than 70 of the world’s top financial institutions, Bitvore provides the precision intelligence capabilities top firms need to counter risks and drive efficiencies with power of data-driven decision making.

Uncover rich streams of risk and ESG insights from unstructured data that act as the perfect complement to the internal data and insights your firm is already generating. Our artificial intelligence and machine learning powered system provides the ability to see further, respond faster, and capitalize more effectively.

To learn how the Bitvore solutions can help your organization contact info@bitvore.com or visit www.bitvore.com.